Palm Beach Island Closed 2025 Reinforcing Structural Strength

As 2025 closed, the national economy remained on stable footing. Growth moderated to a more sustainable pace, inflation continued to ease, and recession risks receded. Productivity gains, particularly from AI and broader technology adoption, helped offset the impact of elevated interest rates, while labor market cooling unfolded in an orderly manner rather than a disruptive one. Heading into 2026, economic conditions support cautious optimism, with economic resilience intact and policy developments remaining the primary variable to watch.

Locally, Palm Beach Island closed the year with decisive strength. The single-family market surpassed $2.0 billion in total sales volume, marking only the third time on record this threshold has been reached, alongside 2020 and 2022. Midtown condominiums similarly exceeded expectations, finishing the year with nearly an 80 percent increase in dollar volume compared to 2024. Pricing remained firmly supported by sustained demand, highlighted by Palm Beach’s highest residential sale on record — an off-market oceanfront transaction exceeding $177 million earlier in the year.

The way 2025 closed is consistent with the path outlined in my 2026 Palm Beach market outlook, reinforcing confidence in the market’s underlying structure.

Ultra-Luxury Capital Deployment Continues to Reshape Market Expectations

According to The Wall Street Journal, the top ten residential transactions in the United States all exceeded $100 million for the first time on record. This milestone underscores a structural shift in how ultra-high-net-worth buyers deploy capital. Pricing levels once considered extraordinary are increasingly functioning as benchmarks rather than outliers within the global ultra-luxury segment.

This Q4 analysis builds on trends first outlined in my Q3 2025 Palm Beach market update, where early signs of selectivity and pricing discipline began to emerge.

Florida sat squarely at the center of ultra-luxury activity as 2025 closed. On Palm Beach Island, record year-end pricing and landmark transactions earlier in the year, including an off-market oceanfront sale exceeding $177 million, underscore a market shaped by capital depth, structural scarcity, and intent rather than momentum or speculation.

Wealth Migration and Institutional Expansion Continue to Drive Demand

Momentum continues to coincide with sustained relocation activity from high-tax states, particularly California, as ultra-high-net-worth individuals respond to evolving fiscal and regulatory environments. Increasingly, these buyers are drawn not only by Florida’s tax advantages, but also by proximity to global financial, technology, and innovation networks alongside privacy, security, and permanence.

Population and capital inflows also continue strengthening Palm Beach County’s appeal as a long-term destination for both investment and talent. Institutional commitments from organizations including Vanderbilt University, ServiceNow, and Wells Fargo’s wealth management platform underscore a structural shift toward sustained economic activity throughout the region.

While Palm Beach Island remains distinct in character and scale, its proximity to this expanding innovation corridor provides economic diversification without sacrificing exclusivity — qualities that continue to resonate with senior executives relocating to Palm Beach County.

Palm Beach Island's Defining Characteristic: Supply Constraint

What distinguishes Palm Beach Island is not transaction velocity but market structure. Limited land availability, restrictive development, and high seller discretion continue constraining supply, while sustained inflows of long-term capital reinforce demand. The result is a market that moves deliberately, with fewer but more consequential transactions.

This dynamic increasingly rewards quality over optionality. Renovated, well-located, turnkey residences continue commanding attention and transacting decisively, while assets requiring compromise often experience longer decision cycles. Selectivity is not slowing the market — it is shaping how and where transactions occur.

Taken together, the way 2025 closed offers a clear signal rather than a forecast. Palm Beach Island continues operating on its own cadence, shaped by deep capital, structural constraints, and intentional decision-making.

Inventory

Single-Family Homes

At the end of Q4 2025, there were 114 active single-family listings in the MLS. Based on the year’s absorption rate, this represents approximately a 12-month supply, effectively one season of inventory.

While inventory increased modestly year over year, it remains 37 percent below pre-pandemic Q4 2019 levels, reinforcing the structural constraints that continue to define supply at the upper end of the market.

Midtown Condominiums and Co-Ops

Midtown ended Q4 with 89 active listings, representing an approximate 10-month supply.

Inventory increased slightly year over year but remains roughly 30 percent below pre-pandemic levels. This measured pace of inventory growth, combined with seller discretion, has supported pricing stability, particularly for renovated, turnkey residences offering walkability and ease of ownership.

South End Condominiums and Co-Ops

The South End closed the quarter with 121 active listings, equating to an approximate 15-month supply.

Inventory declined 12 percent from Q4 2024 and remains 28 percent below pre-pandemic norms, contributing to firmer pricing for compliant and upgraded properties despite ongoing inspection and assessment considerations.

Transactions

Single-Family Homes

Q4 2025 recorded 26 transactions, a 37 percent increase over Q4 2024, and the strongest fourth-quarter performance since 2021.

For the full year, 119 single-family sales closed, up 31 percent year over year. The year ended with 14 properties under contract, totaling approximately $260 million in combined asking volume, a 35 percent increase compared to year-end 2024.

Midtown Condominiums and Co-Ops

Midtown posted 16 Q4 transactions, up 23 percent year over year.

For the full year, 104 transactions closed, representing a nearly 50 percent increase from 2024. Demand remained concentrated among buyers seeking turnkey, low-maintenance, well-located residences that support seasonal or part-time living.

South End Condominiums and Co-Ops

The South End recorded 18 transactions in Q4, up 38 percent year over year.

Despite the strong fourth quarter, full-year transactions declined 11 percent, reflecting buyer selectivity tied to building condition, assessments, and compliance requirements.

Dollar Volume and Pricing

Single-Family Homes

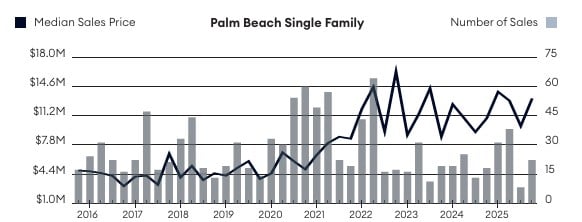

Q4 single-family dollar volume totaled $436 million, a 44 percent increase year over year. Full-year dollar volume exceeded $2.1 billion, marking only the third time on record Palm Beach Island has surpassed this level.

The Q4 median sale price reached $12 million, up 14 percent year over year, representing the second-highest Q4 median on record. The 2025 year-end median price of $13 million increased 16 percent from 2024, the highest year-end median ever recorded.

Notably, 62 percent of Q4 transactions and 67 percent of full-year sales closed at or above $10 million, underscoring the depth of capital at the upper end of the market.

Midtown Condominiums and Co-Ops

Q4 Midtown dollar volume totaled $46 million, modestly below Q4 2024, though full-year dollar volume reached $407 million, a 78 percent increase year over year and the third-highest year on record.

The Q4 median price of $2.4 million rose 2 percent year over year, while the 2025 year-end median of $2.9 million marked the highest year-end median on record.

South End Condominiums and Co-Ops

South End dollar volume reached $38 million in Q4, up 72 percent year over year. Full-year dollar volume totaled $182 million, down 7 percent from 2024, reflecting softer activity earlier in the year.

The Q4 median price of $1.2 million declined 9 percent year over year, while the 2025 year-end median of $1.35 million finished 1 percent higher than 2024, highlighting underlying value support for compliant properties.

What This Market Means for Buyers

Entering 2026, Palm Beach Island continues to reward preparation, clarity of acquisition goals, and patience in evaluating opportunities. While competition remains strong for premier turnkey properties and prime waterfront estates, the current environment allows buyers to conduct more comprehensive due diligence and structure transactions thoughtfully.

Buyers who want a deeper understanding of navigating acquisitions on Palm Beach Island may find this guide helpful:

How to Buy a Luxury Home in Palm Beach

(Keep existing link)

What This Market Means for Sellers

Palm Beach Island continues providing exceptional pricing support for sellers, particularly for properties aligned with current buyer expectations. However, transaction success increasingly depends on strategic pricing, presentation quality, and precise positioning within the competitive landscape.

Turnkey properties and architecturally significant estates tend to generate stronger engagement, while homes requiring renovation benefit from targeted marketing strategies and thoughtful pricing alignment.

Frequently Asked Questions About the Palm Beach Island Market

How are Palm Beach Island home prices trending?

Palm Beach Island home prices have historically demonstrated strong long-term appreciation, supported by limited land availability, sustained global wealth migration, and deep capital demand. Over roughly the past decade, the median single-family sale price has more than tripled, reaching pricing levels above $17 million during recent market cycles. While individual quarters can show variability, long-term pricing patterns continue to trend upward, reinforcing Palm Beach Island’s role as a supply-constrained global luxury market.

Palm Beach Island Median Single-Family Sale Price (Long-Term Trend)

Long-term pricing data illustrates sustained appreciation on Palm Beach Island, supported by structural scarcity and global demand rather than short-term market cycles. Source: Miller Samuels

Is Palm Beach Island real estate demand slowing?

Demand remains strong but has become more deliberate. High-net-worth buyers continue to actively pursue Palm Beach Island properties, particularly turnkey and waterfront estates. What has evolved is the pace of decision-making. Buyers are spending more time evaluating property condition, renovation feasibility, and long-term lifestyle alignment, which reflects market maturity rather than declining interest.

Is inventory increasing on Palm Beach Island?

Inventory has increased modestly in certain segments compared to recent pandemic-era lows, but it remains significantly below long-term historical levels. Palm Beach Island’s geographic constraints, preservation standards, and high seller discretion continue to limit new supply. These structural limitations help support pricing resilience and contribute to the Island’s long-term scarcity-driven market dynamics.

What types of properties are performing best on Palm Beach Island?

Turnkey, renovated, and architecturally distinctive properties continue to command the strongest buyer attention. Homes offering premier waterfront locations, walkability, or exceptional design tend to transact more decisively. Properties requiring renovation or repositioning can still attract strong interest but often involve longer decision cycles and more strategic pricing.

Is now a good time to buy on Palm Beach Island?

For buyers focused on long-term ownership, Palm Beach Island continues to present compelling opportunities. The current environment often allows buyers to evaluate properties more carefully, conduct thorough due diligence, and negotiate transaction structure and timing more thoughtfully. Buyers entering the market with clear acquisition goals and strong preparation are typically best positioned to capitalize on opportunities.

Why is Palm Beach Island considered a supply-constrained market?

Palm Beach Island is physically limited by geography and tightly regulated development standards. Preservation priorities, zoning restrictions, and high seller discretion significantly restrict new housing inventory. Combined with sustained demand from domestic and international wealth migration, these constraints create a market environment where supply remains structurally limited and pricing is strongly influenced by scarcity.

What should sellers know before listing on Palm Beach Island?

Sellers continue to benefit from strong pricing support, but successful outcomes increasingly depend on preparation and positioning. Strategic pricing, thoughtful presentation, and understanding how a property compares to competing inventory are critical. Properties aligned with current buyer preferences tend to attract stronger engagement and shorter marketing timelines, while homes requiring updates benefit from targeted marketing strategies and clear pricing alignment.

Closing Perspective

Palm Beach Island’s luxury real estate market continues to be defined by confidence, capital depth, and structural scarcity. As 2025 concluded, market performance reinforced a consistent pattern: pricing strength supported by sustained global demand, balanced by increasingly thoughtful and intentional transaction pacing.

Rather than following broader housing cycles, Palm Beach Island continues to operate within its own rhythm, shaped by limited supply, long-term capital inflows, and buyers prioritizing lifestyle alignment and wealth preservation.

For buyers and sellers alike, understanding how these structural forces influence pricing, negotiation strategy, and opportunity timing remains central to making confident real estate decisions.

If you are considering buying or selling on Palm Beach Island, I welcome the opportunity to provide perspective tailored to your goals.

Nadine Fite

Luxury Real Estate Advisor | Palm Beach Island

📧 [email protected]

📱 917.513.9592

🌐 LivePalmBeach.com

📍 Compass Palm Beach | 150 Worth Avenue, Palm Beach, FL 33480

Follow along: @Nadine_Fite_PBRealtor

#LivePalmBeach