Palm Beach Luxury Real Estate: A Market That Moves Differently

The Palm Beach luxury real estate market continues to distinguish itself from broader national housing trends. Driven by sustained wealth migration, limited supply, and lifestyle-led demand, pricing and buyer behavior here reflect a market shaped more by long-term alignment than short-term cycles.

While national housing conversations often center around interest rates and affordability pressures, Palm Beach operates within a different framework. Buyers entering this market are typically influenced by tax strategy, generational wealth planning, business relocation, and lifestyle priorities — forces that create a demand profile less sensitive to traditional housing cycles.

Understanding the Palm Beach market in 2026 requires viewing it through that broader structural lens.

Palm Beach Island as the Prestige Anchor — With County-Wide Opportunity

Palm Beach Island continues to serve as the global brand center of the market. Its limited inventory, historic architectural character, oceanfront exclusivity, and international visibility maintain its role as the region’s pricing benchmark and prestige anchor.

At the same time, Palm Beach County has evolved into a dynamic luxury ecosystem offering a wider range of property types, amenities, and lifestyle options. Communities throughout the county increasingly attract buyers seeking access to the Palm Beach lifestyle while prioritizing flexibility, value alignment, and long-term usability.

Rather than functioning as competing markets, Palm Beach Island and Palm Beach County operate as complementary components of a unified luxury landscape.

Palm Beach Island and Palm Beach County: A Unified Luxury Market

Palm Beach Island remains the prestige anchor of the market, recognized globally for its oceanfront estates, historic architecture, and limited inventory. Surrounding Palm Beach County communities offer a broader range of luxury opportunities across price points, property types, and lifestyle preferences. Together, they form a connected luxury ecosystem that continues to attract both domestic and international buyers.

The Structural Drivers Sustaining Demand

Several long-term forces continue to support Palm Beach luxury real estate:

Wealth Migration and Capital Preservation

Migration from high-tax states and global financial centers remains a primary demand driver. Many buyers relocating to South Florida are making long-term residence decisions that align with tax strategy, estate planning, and generational wealth considerations.

Financial and Corporate Expansion

The continued expansion of financial services, hedge funds, private equity firms, and family offices has deepened the region’s buyer pool. West Palm Beach, in particular, continues to strengthen its position as a business and financial hub, reinforcing residential demand across multiple luxury tiers.

Lifestyle Permanence

Palm Beach is increasingly viewed as a year-round destination. The region’s cultural and social landscape has long supported this lifestyle and is now being recognized more broadly, which I explore further in Palm Beach’s Art & Culture Season. Expanded seasonal offerings and community experiences continue to attract residents and visitors alike, reinforcing Palm Beach’s reputation as a dynamic and enduring destination beyond the typical seasonal narrative.

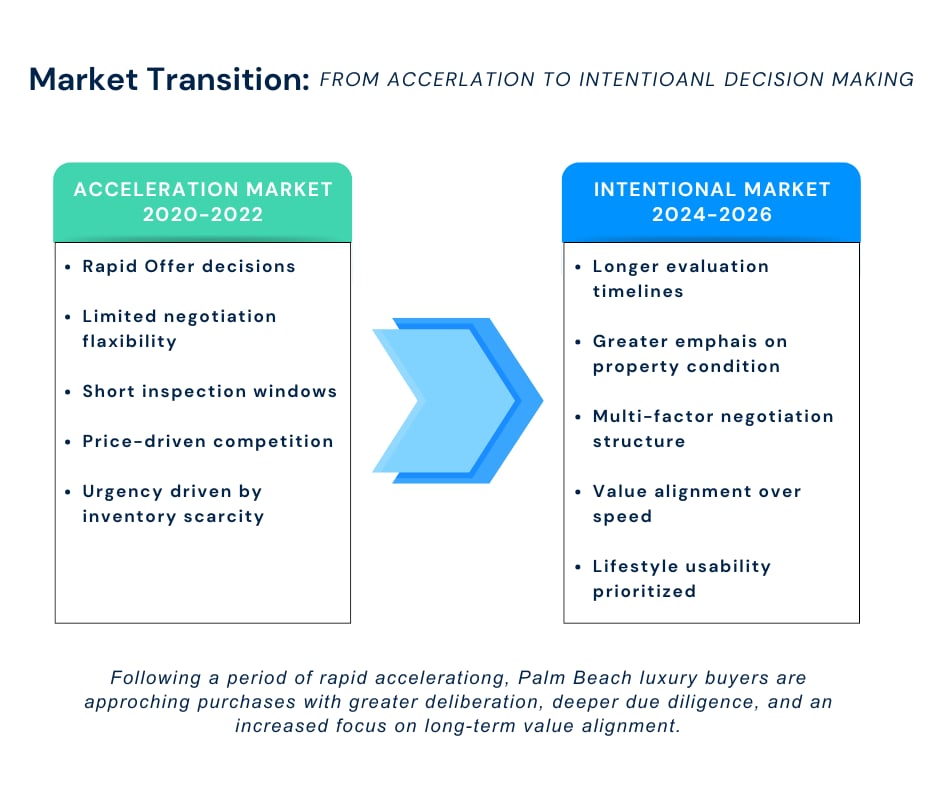

Transaction Patterns Reflect a Maturing Market

The most noticeable evolution entering 2026 is not demand itself, but how transactions unfold.

Buyers remain active while approaching acquisitions with greater deliberation. Decision timelines have lengthened modestly as buyers evaluate property condition, renovation potential, long-term usability, and lifestyle alignment alongside pricing considerations.

Sellers continue to benefit from strong pricing support, though success increasingly depends on presentation, strategic positioning, and precise market alignment. Properties that meet current buyer expectations tend to attract strong engagement and efficient transaction timelines, while homes requiring repositioning may experience longer marketing periods.

These patterns reflect a market that is maturing rather than slowing.

Palm Beach luxury transactions have evolved from rapid, urgency-driven decision making toward a more deliberate acquisition process focused on long-term value, property condition, and lifestyle alignment.

Pricing Stability and Long-Term Market Resilience

Long-term pricing trends reinforce the structural strength of the Palm Beach market, building on patterns I first outlined in my recent Palm Beach market update, where early signs of increased buyer selectivity and pricing discipline began to emerge.

Luxury pricing historically demonstrates the ability to accelerate during periods of heightened demand while maintaining relative stability during normalization phases. This behavior reflects wealth-driven purchasing patterns and persistent supply limitations that differentiate luxury housing from broader residential cycles.

The result is a market that tends to adjust through negotiation and selectivity rather than broad price contraction.

New Development Driving Palm Beach County Luxury Expansion

New development continues to shape inventory and attract evolving buyer segments. Projects including Olara, The Ritz-Carlton Residences West Palm Beach, Mr. C Residences, and other emerging developments are introducing product types that appeal to buyers seeking turnkey luxury living with modern amenity packages.

While these developments expand buyer choice, they do not fundamentally alter the long-term supply constraints that continue to support pricing strength throughout the region. For a broader look at new residential offerings across Palm Beach County, you can explore current development opportunities on LivePalmBeach.com.

Emerging luxury condominium developments in West Palm Beach continue to attract new buyer segments while expanding lifestyle and inventory options across the county.

What This Market Means for Buyers

Buyers entering the Palm Beach luxury market in 2026 are operating within an environment that rewards preparation, clarity of priorities, and strategic decision-making. For those seeking a deeper understanding of how to navigate acquisitions in this market, this guide may be helpful: How to Buy a Luxury Home in Palm Beach.

Competition remains strong for highly desirable properties, though the pace of transactions often allows more opportunity to evaluate property condition, renovation potential, and long-term usability. Off-market opportunities and flexible transaction structures are increasingly important components of successful acquisition strategies.

Entering the market with clearly defined goals and strong preparation typically leads to more confident and effective decision-making.

What This Market Means for Sellers

Palm Beach continues to provide strong pricing support for sellers, particularly for properties that align with current buyer expectations. However, successful transactions increasingly depend on thoughtful preparation, pricing precision, and presentation quality.

Today’s buyers are highly informed and selective. Turnkey homes or properties positioned clearly within the competitive landscape typically generate stronger engagement. Homes requiring renovation or repositioning can still perform well but benefit from strategic pricing and targeted marketing.

Sellers who approach the market with preparation and flexibility remain best positioned for successful outcomes.

Frequently Asked Questions About the Palm Beach Luxury Market

Is the Palm Beach luxury market slowing down?

Demand remains strong, though buyer decision-making has become more deliberate. Transactions may take longer to complete, reflecting careful evaluation rather than declining interest.

Are luxury home prices expected to decline?

Long-term data shows Palm Beach luxury pricing tends to stabilize during transitional periods rather than experience broad declines. Individual property performance continues to depend heavily on pricing strategy, condition, and market positioning.

Is inventory increasing in Palm Beach County?

New development is expanding inventory options, particularly in condominium and turnkey living categories. However, land limitations and zoning constraints continue to restrict large-scale supply expansion, particularly on Palm Beach Island.

Is 2026 a good time to buy luxury property in Palm Beach?

For buyers focused on long-term ownership, the current market often provides opportunities to evaluate properties more thoroughly and negotiate transaction terms thoughtfully.

How should sellers prepare before listing?

Preparation typically includes pricing strategy analysis, property presentation planning, and evaluating how the property compares to competing inventory. Early preparation allows sellers to enter the market from a position of strength.

Closing Perspective

Palm Beach luxury real estate is best understood through the structural forces that shape its unique demand profile. As wealth migration, business expansion, and lifestyle investment continue to influence the region, the market is evolving with clarity and intention.

For buyers and sellers alike, understanding how these dynamics influence pricing, inventory, and negotiation strategy is essential to making confident real estate decisions.

If you’re considering buying or selling in Palm Beach or Palm Beach County in 2026, I’d welcome the opportunity to discuss how these market dynamics intersect with your goals and timing.

Nadine Fite

Luxury Real Estate Advisor

📧 [email protected]

📞 917.513.9592